Frequently Asked Questions (FAQs)

- TOP 10 QUESTIONS

-

- I bought my home last year, and this year the taxes increased dramatically even though I applied for the Homestead Exemption. What happened?

-

Under Florida Law, all exemptions and assessment caps possessed by the prior owner must be removed on the January 1 after a change of ownership. The prior owner was likely benefiting from a Save Our Homes cap benefit that held the Assessed Value of the property well below its Just/Market Value. When you crossed your first January 1 under your ownership the Assessed Value reset to Just/Market Value. We then apply any portability from a prior Florida homestead and any additional exemptions, if applicable.

- My structure was damaged or destroyed, how is it possible that my taxes increased?

-

The longer you own a homesteaded property, the higher the likelihood that your assessed value and taxes may not decrease and have the potential to increase due to the long-time protection provided by the Save-Our-Homes cap. This is a provision of Save Our Homes known as the Recapture Rule. An example of this scenario would be a property where the structure was demolished, but the assessed value is already below its land value due to long-time ownership. Properties acquired within recent years are more likely to see downward movement in their assessed value and property taxes.

- The 2025 FEMA letter shows a lower building value than the 2024 or the Building Value Reconsideration (BVR) I received after the storm. What should I do?

-

- If you experienced storm damage that was not repaired as of January 1, 2025, please use the 2024 (pre-storm) letter or BVR prepared by our office.

- If your home was not damaged or was repaired by January 1, 2025, please use the 2025 FEMA letter. If this letter reflects a lower building value than the 2024 letter, it likely reflects storm damage depreciation. However, if you were not damaged or were repaired by January 1, 2025, please contact our office and ask to speak to your Area Appraiser to discuss so that we can make any warranted adjustments.

- If you completed repairs to your home after January 1, 2025, please use the 2024 letter. However, if there is a damage event that impacts your property during 2025, our office will provide Building Value Reconsiderations (BVRs) for these property owners upon request with good supporting documentation. Owners can always engage a private appraiser. It is imperative to have good photos (not video) of all areas of your home for both appraisal and insurance purposes. These should be taken as repairs progress, as well as at completion.

- Will my property's assessed value increase if I repair or rebuild my home after Hurricane flood damage?

-

No, as long as the property owner maintains the homestead status on the calamity property, and the repaired or rebuilt home does not exceed the property’s statutory calamity allowance based on the structure’s original square footage. Square footage exceeding the allowance will be added to both the Just/Market and Assessed Values as new construction.

Recent legislation passed by the Florida Legislature and signed by the Governor on June 26, 2025, revises the respective calamity allowances as follows:

- Construction completed in 2024 tax year or prior - 110% of the original structure’s living area or 1,500 SF, whichever is greater – applies to both Homestead and Non-Homestead Property

- Construction completed in 2025 tax year or later - 130% of the original structure’s living area or 2,000 SF, whichever is greater – applies to Homestead Property Only

Under Florida Law, if a property is damaged or destroyed by misfortune or calamity after the damage or destruction occurs, the property owner may continue the homestead exemption. The calamity provision in Florida Law protects property owners from an increase in their assessed value following a catastrophe when repairing/rebuilding their property up to the property’s respective calamity allowance based on their original square footage. The owner must notify the Property Appraiser that they intend to repair or rebuild the property. Visit our Repair or Replacement of Damaged or Destroyed Property due to a Calamity webpage for more details.

- If I intend to use the calamity provision, can I apply for homestead elsewhere in the interim as my property is being repaired/rebuilt?

-

No. In order to qualify for the calamity provision described above, the homestead status on the damaged property must not change from the date of the storm through completion of the repairs or rebuild. If the homestead status changes, the ability to utilize the calamity provision is lost.

- After rebuilding/repairing my home, do I need to submit a new Homestead Exemption?

-

No, homeowners may continue to receive the homestead exemption and the Save-Our-Homes cap as long as it is not removed from the property, and they do not claim a new homestead exemption on a different home while they rebuild or repair the damages. Section 193.155 4(b), Florida Statutes

- Why are my taxes increasing when the market value of my home is going down?

-

There are a couple of reasons why this may happen. It may be because the millage rate (tax rate) determined by local taxing authorities is increasing. Another reason may be what's known as the "Recapture Rule". In short, if you have the Save Our Homes cap on your property and your market value decreases, the assessed value will still increase by the annual cap rate until it reaches the just/market value.

- Why did the living area of my home decrease?

-

The living area of my home decreased on the Property Appraiser’s website. What happened?

The 2024 hurricane season brought unprecedented damage to many homes in Pinellas County. It also resulted in a better understanding by Building Officials of how the National Flood Insurance Program (NFIP) works in conjunction with FEMA rules for homes located in a Special Flood Hazard Area (SFHA), which are homes located in Flood Zones A and V. Specifically, homes built in 1975 or later and located in SFHA may not have heated/cooled living area below the Base Flood Elevation (BFE), except for a small area used to access the living areas above BFE from areas below BFE.

In order to distinguish between living and non-living areas of a home, the Property Appraiser uses the term “sub-area” to identify different areas of a home based on level of finish. Examples of sub-areas include: heated/cooled space (BAS), upper story finished (USF), finished garage area (GRF), and many more.

When a home built in 1975 or later and located in a SFHA has finished heated/cooled space that is located below BFE, that area is assigned the LAF (Lower Area Finished) sub-area in the property appraiser’s database. Prior to July 1, 2025, LAF was included in the square foot calculation used to generate a home’s living area in our database. However, after July 1, 2025, LAF was removed from a home’s living area calculation to align with Florida Building Code, FEMA requirements, NFIP criteria, and local building department building codes and permitting requirements.

This practice is consistent with how professional real estate agents and private sector appraisers handle the living square footage when listing and valuing property since the area below BFE is uninsurable.

If the living area assigned to my home is smaller, will I get a tax refund?

In the Property Appraiser’s computer system, the value assigned to the LAF sub-area is not changing as it carries contributory value; therefore, no refund is needed. The LAF sub-area is still part of the gross area of the structure and was already valued at less than the base living area. If your value changed this year from the previous year, it was due to other factors such as an additional year of depreciation, special storm depreciation related to storm damages or other calamity, a change to the model used to value residential properties, or a change in market conditions such as higher or lower sale prices of similar properties. If your lower level was finished as conditioned space pre-storm but was returned to only parking, storage, or access after repairs, please call our office at (727) 464-3207 and ask for your Area Appraiser so that we can make the appropriate adjustments.

How do I request this area to be changed?

Your Area Appraiser is here to help and is glad to review any pertinent documentation you can provide. The primary source of information is found on an Elevation Certificate (EC) issued by a survey company, which shows the Base Flood Elevation (BFE) and the lowest finished floor height of the subject property. This is typically labeled as the “Top of bottom floor” on an EC. Another potential document that may show this information would be the architectural plans. Supporting documentation that the LAF was built above the BFE at the time of original construction would allow us to move this area back into the living area calculation. Also considered would be a letter from the Chief Building Official in your local jurisdiction stating that the LAF in question could be legally permitted for repairs as finished living space in the event of a future calamity and is insurable through the National Flood Insurance Program (NFIP).

A portion of the LAF is actually used as access to the upper floor(s). Can I have my Area Appraiser measure this area to reflect the portion that is used to access the upper stories?

Yes, your Area Appraiser would be glad to assist in remeasuring the LAF. The re-measurement will require architectural plans or an inside inspection of the LAF area to determine the size of the area used for access, which is typically added to the total living area. You may contact our office at (727) 464-3207 to schedule an inspection. If you have a copy of the architectural plans in PDF format, you can email those to our office at mike@pcpao.gov. Please include your contact information and the parcel number in the email together with your request.

Resources to Assist in Verifying if LAF was compliant at time of construction:

1. Check for an Elevation Certificate (EC) on the pcpao.gov website:

- The above EC information is pulled from the Pinellas County Enterprise GIS system: https://pinellas-egis.maps.arcgis.com/apps/webappviewer/index.html?id=c66f8a2216d34a49a9675ecaf134a61a

2. Historical Flood Insurance Rate Maps (FIRMs) can be found at the FEMA Flood Map Service Center: https://msc.fema.gov/portal/advanceSearch

- This is helpful when trying to identify what the legal BFE was at the time of original construction.

- Do you have a copy of my land survey?

-

No. Contrary to popular belief, land surveys are not filed with the Property Appraiser's office. A land survey is a document created by a surveyor that identifies the boundaries, rights of way, easements and location of existing improvements. While often mistaken for a survey, the maps displayed on our website and maintained by our office are for the purpose of maintaining the property assessment roll and should not be relied upon as a substitute for a survey.

Since survey's are typically required by lenders during the transfer of property, property owners are encouraged to contact the title company that handled the title transfer for their acquisition of the property, or the mortgage lender if their purchase was more than 3 years ago.

- What do I need to know when buying or selling a home?

-

Before you buy a home in Pinellas County, our tax estimator will help you know what your property taxes may be under your ownership. You may also be eligible for homestead or personal exemptions that will help to reduce your property taxes.

When you sell your Florida home, your exemptions do not automatically transfer to a new property. You must apply for a new exemption on your next primary residence. Also, if your previous home had the Homestead Exemption, and its assessed value was capped under Save Our Homes, you may be able to “port” (transfer) that savings benefit to your new Florida homestead.

Please visit our webpage: https://www.pcpao.gov/Learn-About/Buying-or-Selling-a-Home for further information.

- TECHNICAL QUESTIONS

-

- Why can’t I print?

-

Users may occasionally need to disable their browser’s pop-up blocker in order to print from our website or get access to information that pops up in a new window. Often users are not aware the browser is stopping them from viewing content.

It is impossible for our office to know if the user has turned pop-up blockers off (or on) within the settings in their browser. The following instructions may help you disable pop-up blockers but note that these processes may change without our knowledge.

How to Disable Pop-Up Blocker: Chrome (Desktop)

- Open your Chrome browser

- In the upper right-hand corner, click the three vertical dots, then select “Settings”

- At the bottom of the menu, click “Advanced”

- Scroll down to “Privacy and security,” and select “Site Settings”

- Select “Pop-ups and redirects”

- At the top of the menu, toggle the setting to “Allowed” to disable the pop-up blocker

How to Disable Pop-Up Blocker: Firefox (Desktop)

- Open your Firefox browser

- Click the “Menu” button, then select “Options”

- Select “Privacy & Security”

- Under “Permissions”, uncheck “Block pop-up windows” to disable the pop-up blocker

How to Disable Pop-Up Blocker: Edge (Desktop)

- Open your Microsoft Edge browser

- Go to “Settings”, then select “more > Settings > Privacy & security”

- Under “Security”, switch “Block pop-ups” to off to disable the pop-up blocker

How to Disable Pop-Up Blocker: Safari (Mac)

- Select Safari > “Preferences”, then select “Websites”

- Select “Pop-up Windows”

- Use the “When visiting other websites” drop-down menu and select “Allow” to disable the pop-up blocker

How to Disable Pop-Up Blocker: iPhone/iOS

Safari for iOS:

- On your iOS device, open the “Settings” menu

- Select “Safari”

- Slide “Block Pop-ups” to off (white) to disable pop-up blocking

Chrome for iOS:

- On your iOS device, open the Chrome app

- Tap “More” > “Settings” Tap “Content Settings”, then tap “Block Pop-ups” Turn Block Pop-ups “off” to allow pop-ups

How to Disable Pop-Up Blocker: Android

Chrome:

- On your Android device, open the Chrome app

- Tap “More” > “Settings”

- Tap “Site settings”, then “Pop-ups and redirects”

- Turn Pop-ups and redirects “on” to allow pop-ups

Samsung Internet:

- On your Android device, open the Samsung Internet app

- Tap the Menu icon (three vertical lines)

- Select “Settings”

- Under “Advanced”, tap “Sites and downloads”

- Slide “Block Pop-ups” to off (white) to disable pop-up blocking

Firefox:

There is currently no way to access the pop-up blocker settings in Firefox for Android.

- Why does my property detail print preview look different from the webpage?

-

There may be an optional check box required that cannot be automatically activated in some web browsers. Enabling background graphics will make the printout appear similar to the web page. While the print dialog box is open, click “More settings”, then “Options” and check the background graphics box to activate. This box is checked by default in Chrome, Internet Explorer and Firefox. Other options are to choose a different printer; print to PDF; or try using a different browser such as Firefox, Edge (replacing Internet Explorer), Chrome, or DuckDuckGo.

- Why doesn't the parcel map display on the property detail page?

-

This is typically a result of one of the following issues:

1) Web browsers tend to hold onto information (cookies), which over time could cause issues with logging in or displaying websites correctly. If you are experiencing issues with the parcel map loading on a property detail page, you may need to clear your web browsing cache/history, then close and restart your web browser.

2) Antivirus software may mistakenly suspect ‘malware’ and block viewing. Please white list the file named ‘js.arcgis.com’ in your antivirus software.

3) Enable Background Graphics is turned off - If printing, enabling background graphics will make the printout appear similar to the web page. While the print dialog box is open, click “More settings”, then “Options” and check the background graphics box to activate.

If you are still experiencing issues afterward, please contact our Mapping Department at (727) 464-3207 for assistance.

- Why does the map say my location is somewhere different than where I actually am?

-

This feature is intended to be used on a mobile device (smart phone or tablet) with location services enabled. User experience varies on desktop computers. If you receive your desktop computer internet service from an ISP (internet Service Provider), then you are likely to be placed in the wrong location. The last location that is sent back is the last building/terminal of your ISP before it reaches you. This could be miles away from your actual location or even in another state.

- I found a data error on your website, who should I contact?

-

We appreciate your time in helping us correct erroneous data. Please submit a detailed note using the Contact Us/Questions Comments Suggestions section of our website. Be sure to include your contact information so we may discuss if we determine there is a misunderstanding and data does not need to be changed.

- SEARCH QUESTIONS

-

- Can you tell me who owns property located at…?

-

The Quick Search feature on our Home page will display data for a parcel within Pinellas County. Search by address, name or parcel number.

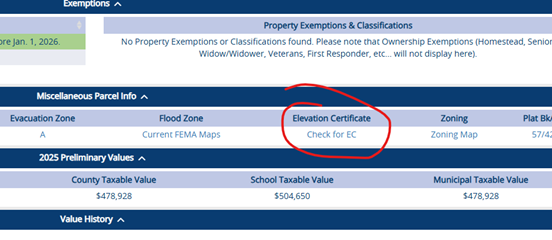

- Where do I find my Elevation Certificate?

-

Our office does not maintain elevation certificates (EC), but if publicly available in County records, they can be found on your property detail webpage.

Search for your property, then scroll down your Parcel Detail page until you locate the Miscellaneous Parcel Info section. Click on the link titled “Check for EC” under Elevation Certificate.

The above EC information is linked to the Pinellas County Enterprise GIS system: https://pinellas-egis.maps.arcgis.com/apps/webappviewer/index.html?id=c66f8a2216d34a49a9675ecaf134a61a

If you have a completed certificate, you can upload your certificate to the Florida Division of Emergency Mgmt (FDEM) website at: https://www.floridadisaster.org/elevation-certificates/

If an EC needs to be completed, please contact a state-licensed surveyor, architect, or engineer to complete one for you, and request they submit it to FDEM on your behalf.

For more information about elevation certificates, please contact the Floodplain Administrator in your municipality, or if in unincorporated Pinellas, call (727) 464-7700 or visit https://pinellas.gov/flood-elevation-certificate/

- What is the best way to search for an address?

-

Often, "less is more" when it comes to searching. Entering just the street number and street name in the address search field will return addresses with those criteria.

Street suffixes are abbreviated in our database. E.g., "Street" (St), "Avenue" (Ave), "Boulevard" (Blvd), “Parkway” (Pkwy), “Lane” (Ln), etc.

Street names that contain words that would normally be considered a street suffix, are not abbreviated. E.g., World Parkway Blvd.

Unusual addresses:

STREET NAME: ENTER: County Rd (CR) County Road State Rd (SR) State Road Alternate US Highway 19 Alt 19 US Highway 19 US 19 Martin Luther King addresses are municipality specific:

IF THE PARCEL LIES IN: ENTER: Clearwater / Largo / Dunedin Martin Luther King Jr Ave Safety Harbor Dr ML King Jr St N St Petersburg Dr Martin Luther King Jr St Tarpon Springs Martin Luther King Jr Dr Unincorporated Clearwater/Largo Dr Martin Luther King Jr Ave - Why isn't zoning displayed on the property record?

-

Pinellas County is home to 24 incorporated municipalities plus the unincorporated areas, each with their own zoning regulations. Tracking and maintaining changing zoning information would most likely lead to inaccurate and/or out of date information. However, we do provide a link to the respective jurisdiction's zoning map on the property info pop-up on the Map Search page. This link will take you to the level of the online resource available for public use that we are able to connect to. For example, in larger jurisdictions such as St. Petersburg, Clearwater, and Unincorporated Pinellas County, we are able to take you to the parcel level within the jurisdiction's mapping system. However, smaller jurisdictions, such as some of our beach towns, only have a PDF zoning map depicting their entire town (will require you to visually search the map for your parcel of interest).

We advise any zoning questions be directed to the municipality in which the property is located, or the Pinellas County Building Department webpage if the property lies in an unincorporated area.

- Why aren't the number of bedrooms and bathrooms listed?

-

Bedrooms are not listed because all measurements are taken from outside the home and specific rooms are not detailed. The mass appraisal method, which is used by Florida’s Property Appraisers, uses square footage, not the number of rooms, as one of the criteria when valuing property.

Bathrooms are expressed in terms of fixtures. A fixture is the hole through which water runs. Examples of fixtures are sinks, toilets, stall shower, tub, tub/shower combo, kitchen sink, water heater, outside spigot and laundry hook-up. A kitchen sink, water heater, laundry hookup and outside spigot are typical fixtures in a residence already included in the base rate, therefore are not included in our fixture count. Examples of fixtures that are over the base rate are:

- 1/2 Bath = 2 fixtures: toilet and sink.

- 3/4 Bath = 3 fixtures: toilet, sink, and bathtub or shower*.

- Full Bath = 3-5 fixtures: toilet, 1 or 2 sinks, bathtub and/or shower*.

A higher fixture count increases the cost to build the residence.

*Add an extra fixture if the bathtub and shower are separate.

- Where will I find a copy of a deed?

-

Start by searching pcpao.gov for the property by address, owner name, or parcel id. Once on the property detail webpage, scroll down to the Miscellaneous Parcel Info section. Click on the link underneath Last Recorded Deed to view the document. You can also scroll further down the property detail webpage to the Sales History section, which lists all prior owners and the applicable Book/Page link to the deed.

All deeds are recorded by Ken Burke, Pinellas County Clerk of the Circuit Court and Comptroller's Office where you may also view the official records.

If you are searching for a recently recorded deed, we recommend searching the Clerk's website first. Newly recorded deeds can take 4-6 weeks to appear on pcpao.gov. Any questions that arise while viewing the Clerk's recorded documents should be directed to the Clerk's office at (727) 464-7000.

- How do I find a previous owner's name?

-

Our office monitors current ownership but often shows both the grantor and grantee in the Sales History portion of the Property Detail page for transactions within recent years. Prior owners can also be found by searching the current and former deeds associated with the property. Click on the icon to the right of the Book/Page number, which will link you to the Pinellas County Clerk of the Circuit Court official records, where you may view the document and see all parties involved in a particular transaction. Any questions that arise while viewing deeds or other Clerk documents should be directed to the Clerk's office at (727) 464-7000.

- How do I get an address assigned to my property?

-

The Pinellas County Property Appraiser's Office has no authority in the assignment of property addresses. A site address assignment is generally a task of the planning/zoning/development review office having jurisdiction over the subject property. When a new construction building permit is approved by the jurisdiction, a site address is established by the assigning agency.

To locate the jurisdiction presiding over the subject property, use our Property Search feature to locate the property's detailed information page. The jurisdiction is listed in the Parcel Summary section on the site address line. For your convenience, click on Tax Districts in Pinellas County to find a link to each jurisdictions' website.

- OWNERSHIP CHANGES WITH HOMESTEAD QUESTIONS

-

- Will I Lose My Homestead Exemption If I Add Someone To My Deed?

-

Adding names to the ownership of your home normally does not change your Homestead Exemption, however you may lose all or part of the protection your property receives from the Save Our Homes (SOH) assessment limitation or "cap" (see the next FAQ for more details).

The SOH cap keeps the Assessed Value (not the taxes) of your home from increasing more than 3% per year as long as you maintain your Homestead Exemption. A loss of protection from the SOH cap will increase the amount of property taxes you pay.

- Will I Lose My Save Our Homes Cap If I Add Someone To My Deed?

-

This depends on how you own the property (the "tenancy"), and if the new owner files for Homestead Exemption on your property.

"Tenancy" is the term used to describe the way property is owned, the relationship between the owners, and what happens to the property when an owner dies. The most common forms of tenancy are:

- Tenancy by the Entireties,

- Joint Tenants with Right of Survivorship,

- Tenants in Common.

If two or more people own property with a homestead exemption, the type of tenancy that appears on the deed can have an effect on the Save Our Homes (SOH) provision, and ultimately the amount of taxes that are owed.

- If the new owner is your Spouse, or someone who is legally or naturally dependent on you, they must apply for homestead exemption. Your current SOH cap will not be adjusted.

- If the new owner is added as a Joint Tenant with Right of Survivorship, and they DO NOT apply for Homestead Exemption, your SOH cap WILL NOT be adjusted. If they DO apply for Homestead Exemption, your SOH cap WILL be reset to Market Value the following year. In future years, the SOH Cap will protect 100% of the property.

- If the new owner is added as a Tenants in Common and DOES NOT apply for homestead exemption, your SOH cap WILL BE adjusted to protect only your proportionate or "percent" interest in the property. The "percent" interest of any owner who does not have homestead exemption will be assessed at market value each year. If the new owner DOES apply for Homestead Exemption, your SOH cap WILL BE reset to Market Value the following year.

- If you execute a deed where you retain a life estate or enhanced life estate (lady bird deed) your SOH cap WILL NOT be adjusted. By retaining a life estate or enhanced life estate interest in your property you retain the requisite title to the property where it will not affect your SOH cap. However, when you pass away, the remainderman listed on your life estate does not keep the SOH cap you had.

It is important to note, if the new owner is living with you and intends to make the property their permanent residence, it may make financial sense for them to apply for their Homestead Exemption now rather than waiting until a later date. Your Homestead Exemption and SOH cap protects only you, and not the new owner. In the future if you no longer reside in this home, the new owner will have to apply at that time, and the property value and taxes will most certainly be much higher than they are now.

- Can Someone "Inherit" The Save Our Homes Value When Inheriting A Family-Owned Property?

-

In general, a person cannot "inherit" another's homestead exemption or Save Our Homes (SOH) cap benefit, even if they inherit the property. When property changes ownership after the death of the homesteaded owner, the deceased's exemption is removed at the end of the year. The new owner must file for their own exemption once they have ownership of the home.

There are two exceptions that allow someone to "inherit" an existing SOH cap benefit:

- A surviving spouse may retain the existing SOH cap, even if the survivor was not previously on title, so long as the surviving spouse subsequently files for homestead exemption.

- The existing SOH cap may be retained if the person inheriting the property, or being granted a life estate, or beneficial rights under a trust, was naturally or legally a dependent of the deceased AND was permanently residing on the property at the time of the deceased's death. (Section 193.155 (3), Florida Statutes)

In all other instances, the person inheriting the property must file for a new Homestead Exemption.

- Where will I find a copy of a deed?

-

If there is a recorded deed associated with the parcel, view the Property Detail page and locate the Last Recorded Deed listed under Parcel Information. Click on the icon to the right of the Book/Page number, which will link you to the Pinellas County Clerk of the Circuit Court official records website, where you may view the document.

Please note that it may take 2 weeks for newly recorded deeds to show up on the Clerk's website plus an additional 2 weeks to be processed and published to our website. We recommend searching the Clerk's site directly when attempting to locate a recently recorded deed, as this will be the first place it will appear. Any questions that arise while viewing the Clerk's recorded documents should be directed to the Clerk's office at (727) 464-7000.

- How do I find a previous owner's name?

-

Our office monitors current ownership but often shows both the grantor and grantee in the Sales History portion of the Property Detail page for transactions within recent years. Prior owners can also be found by searching the current and former deeds associated with the property. Click on the icon to the right of the Book/Page number which will link you to the Pinellas County Clerk of the Circuit Court official records where you may view the document and see all parties involved in a particular transaction. Any questions that arise while viewing deeds or other Clerk documents should be directed to the Clerk's office at (727) 464-7000.

- Can I "Undo" Or Cancel A Deed That Is Already Recorded?

-

If the wording of your current deed has consequences that you did not intend, you may want to consider a corrective deed. Please consult an attorney, title company or other real estate professional to help you prepare your corrective deed.

It is important to note, a corrective instrument does not act retroactively related to tenancy for the homestead tax exemption and the SOH cap, the tax year begins on January 1 and ends December 31; therefore, we look at the ownership/tenancy of the property each January 1. If a corrective instrument is made in a future tax year, we cannot retroactively make any adjustments to the homestead or SOH cap that may have been affected. The Property Appraiser's Office cannot advise you, since there are many serious considerations that go beyond how homestead exemption is calculated, including income and estate tax consequences. We recommend that you never attempt to change your deed without the help of a professional.

- Are There Other Ways Of Transferring My Property For Estate Planning That Will Not Disturb My Homestead Exemption Or Save Our Homes Cap?

-

Two methods of transferring your property will, in most cases, keep your Homestead Exemption and SOH cap intact: reserve a Life Estate for yourself or transfer your property to your trust. Please consult your attorney or estate planning professional before attempting either option.

If you transfer your property to a trust, your attorney should know that three criteria are required in order for your Homestead Exemption and SOH cap to remain intact:

- You as the homestead owner must have beneficial or equitable title to real property. In other words, you must be the trustee or beneficiary of the trust. If you are the beneficiary but not the trustee, your interest must be in REAL property, not PERSONAL property.

- You must have the present possessory interest in the property. Simply, you must have the right to live there.

- The deed that transfers the property into the trust must be recorded.

- HOMESTEAD EXEMPTION / SAVE OUR HOMES QUESTIONS

-

- What documents do I need to apply for Homestead Exemption?

-

Evidence of residency and qualifications for all owners, including spouses, is required when filing:

- Florida Automobile Registration and Driver License

- Social security numbers for all owners and spouses

- Florida Voter's Registration

- Resident Alien Card or Date of Naturalization, if applicable

- If applying for widow/widower exemption, a death certificate or obituary notice

- Proper certification for a disability exemption

- If applicable, proof of no out-of-state residency-based Exemption Benefits, i.e a letter from the out-of-state appraiser or assessor, or a tax bill.

NOTE: Disclosure of your Social Security Number is mandatory per Section 196.011(1), Florida Statutes.

- Can I transfer my homestead exemption from one home to another?

-

No, a new application for homestead exemption is required at your new Florida residence by March 1 of the application year.

In making this new homestead exemption application, you may also apply for portability to receive any accrued Save Our Homes benefit from your prior FL homestead.

As per Section 196.011(9)(a), Florida Statutes, you no longer qualify for your homestead exemption if:

- Property granted an exemption is sold or otherwise disposed of;

- Ownership changes in any manner;

- The applicant for homestead exemption ceases to use the property as his or her homestead;

- The status of the owner changes so as to change the exempt status of the property.

- What is the Save Our Homes amendment and how does it affect me?

-

The Florida Constitution was amended effective January 1, 1995, to limit annual increases in assessed value of property with Homestead Exemption to 3% or the amount of the Consumer Price Index, whichever is lower. No assessment, though, shall exceed current fair market value. This limitation applies only to property value, not property taxes.

For detailed information visit the Learn About / Save Our Homes page on this website.

- Can I transfer my Save Our Homes benefit from one home to another?

-

On January 29, 2008, Florida voters passed Amendment 1 which included a provision for Portability (transfer) of the Save Our Homes benefit. Visit Learn About / Portability for more information on the Amendment, examples of portability, and to learn about our portability calculator, which is included within our “Tax Estimator”.

- Will I Lose My Homestead Exemption if I add someone to my deed?

-

Adding names to the ownership of your home normally does not change your Homestead Exemption. However, you may lose all or part of the protection your property receives from the Save Our Homes (SOH) assessment limitation benefit or "cap" if the added owner applies for homestead exemption on the property or is added as a tenant in common. The SOH cap keeps the assessed value (not the taxes) of your home from increasing more than 3% per year as long as you maintain your homestead exemption. A loss of protection from the SOH cap will increase the amount of property taxes you pay.

-

Will I lose my Save Our Homes benefit if I add someone to my deed?

-

Possibly, depending on how you own the property (the "tenancy"), and if the new owner files for Homestead Exemption on your property. "Tenancy" is the term used to describe the way property is owned, the relationship between the owners, and what happens to the property when an owner dies. The most common forms of tenancy are:

- Tenancy by the Entireties

- Joint Tenants with Right of Survivorship

- Tenants in Common

If two or more people own property with a homestead exemption, the type of tenancy that appears on the deed can have an effect on the "Save Our Homes" provision, and ultimately the amount of taxes that are owed.

- If the new owner is your spouse, or someone who is legally or naturally dependent on you, they must apply for homestead exemption. Your current Save Our Homes cap will not be adjusted.

- If the new owner is a joint tenant with right of survivorship and DO NOT apply for Homestead Exemption, the SOH cap will not be adjusted.

- If the new owner is a joint tenant with right of survivorship and DOES apply for Homestead Exemption, the SOH cap will be adjusted to market value and start anew the following year. In future years, the SOH Cap will protect 100% of the property. One Important Note! If the new owner intends to make the property their permanent residence, it may make more sense to apply for the new Homestead Exemption now rather than waiting until a later date. The current Homestead Exemption and SOH cap protects only the original owner, not the new owner. In the future if the original owner no longer resides in this home (e.g., moves out and applies for homestead exemption elsewhere or passes away), the new owner will then have to apply for the homestead exemption and the property value and taxes will most likely be much higher than they are now.

- If the new owner is a tenant in common and DOES NOT apply for homestead exemption, the SOH cap will be adjusted to protect proportionately a percentage of interest in the property (e.g., two tenants in common would result in 50% protected, 50% unprotected). The percentage of interest for any owner who does not have homestead exemption will be assessed at market value each year. If the new owner DOES apply for Homestead Exemption, the SOH cap will be adjusted to market value and start anew the following year.

- Can I file for my exemption online?

-

Yes! When you purchase a home, we encourage you to use our convenient online Exemption E-File to apply for exemptions. This easy to use application will step you through the process ensuring you apply for all the exemptions you may be eligible for. You may apply for homestead online as soon as your ownership is reflected on your parcel on our website.

- Is there a deadline to file for an exemption?

-

Yes, the state's deadline is March 1 for the tax year in which you wish to qualify. However, you are urged to file as soon as possible once you own, occupy and make that home your legal residence.

If you received your homestead exemption for the previous year and still occupy, own, and make that residence your permanent home, a receipt will be mailed to you early in January. You only need to notify the Property Appraiser's office if you no longer qualify for these exemptions or if you think you qualify for additional exemptions.

- How do I let my lender know I have an exemption?

-

You may send them either a copy of the Parcel Detail page or the Homestead Exemption Status page for your property from our website.

- How is the Save Our Homes cap treated when demolishing and reconstructing a home with homestead?

-

Option 1 - Property with No Flood History

(a) If there is no flood history on a property, and the owner completely demolishes the property with the intent to rebuild, then the Homestead exemption and Save Our Homes cap (Cap) remain on the land value of the property for the year following the demolition. The property owner must maintain the property as their permanent residence and make reasonable efforts to rebuild. The reconstruction must be finished within three years following the January 1 of the demolition. The value of the new construction will then be added above the Cap once completed.

(b) If the property owner chooses to completely demolish the property with the intent to rebuild, the owner may preserve their Cap on the original improvement by way of Portability. To do this, the property owner must “abandon” the Homestead exemption prior to the demolition of the property. Abandonment of the Homestead exemption will remove the exemption from the land for one year, and allow the property owner two years, including the current tax year, of the demolition to complete rebuilding the home. The owner then must file for Portability through our office by re-applying for the homestead exemption and completing the Portability form (this is a part of the online homestead application). The property must be finished prior to the January 1 of the second tax year. If the property is not finished within this time limit, then the Cap is lost forever.

Option 2 - Property with Documentation of a Flood from Rising Water

The Property Appraiser recognizes private insurers and FEMA document flood claims or repetitive loss flood claims on properties. Your property will be considered damaged by misfortune or calamity if you have a documented flood claim, have been deemed substantially damaged by your local building official, or are designated a repetitive flood loss property by your insurer. In the event of misfortune or calamity, the changes, additions, or improvements to your Homestead property will not increase the assessed value when the square footage of the homestead property as changed or improved does not exceed the calamity allowance percentage based on the property’s square footage of living area before the flood event or the homesteaded property as changed or improved does not exceed the respective calamity allowance square footage, whichever is greater.

Recent legislation passed by the Florida Legislature and signed by the Governor on June 26, 2025, revises the respective calamity allowances as follows:

- Construction completed in 2024 tax year or prior - 110% of the original structure’s living area or 1,500 SF, whichever is greater – applies to both Homestead and Non-Homestead Property

- Construction completed in 2025 tax year or later - 130% of the original structure’s living area or 2,000 SF, whichever is greater – applies to Homestead Property Only

Excess square footage will be added to both the Just/Market and Assessed Values as new construction.

Homestead property owners have 5 tax years from the January 1 following the catastrophic event to pull a building permit to be eligible for the calamity provision. Non-homestead property owners have 3 tax years from the January 1 following the catastrophic event to pull a building permit to be eligible for the calamity provision.

- What other exemptions are available?

-

There are multiple exemptions available to property owners. Please click on Exemptions in the menu bar to learn more. Our friendly customer service representatives are also available and happy to assist you with any questions you may have.

- Can I have homestead in a trust?

-

When property is owned by a trust, a homestead exemption can be granted, but there are strict requirements that must be met in order for the applicant to qualify:

- The applicant must have beneficial or equitable title to real property for life. In other words, the applicant(s) must be the beneficiary of the trust, with interest in REAL property, not PERSONAL property.

- The applicant must have the present possessory interest in the property. Simply, the applicant must have the right to live there, and only the person(s) who has the present possessory interest is entitled to homestead exemption.

- The deed that transfers the property into the trust must be recorded.

If the recorded deed addresses these requirements, we don't need to review the trust document. If the deed does not address these requirements, the trust must be reviewed in order to determine if the applicant is qualified for homestead exemption. Another way to qualify a person for homestead exemption is for the grantor or beneficiary to reserve or retain a life estate on the face of the deed.

Below is sample language that could be included on a deed that would allow a trust beneficiary to qualify for homestead exemption in Pinellas County. Please consult with your attorney or estate planning professional for advice before including this or similar language on the deed that funds your trust.

Grantor(s) reserves the right to reside upon any real property placed in this trust as his or her permanent residence during his or her lifetime. It is the intent of this provision to retain for the grantor(s) the requisite beneficial interest and possessory right in and to such real property for life, and to create “equitable title to real estate.”

Any questions regarding the qualification of trust beneficiaries or trustees for homestead exemption may be directed to the Exemptions Department at (727) 464‐3207.

PLEASE CONSULT YOUR ATTORNEY OR ESTATE PLANNING PROFESSIONAL.

THIS INFORMATION DOES NOT CONSTITUTE LEGAL ADVICE

- PROPERTY VALUE INFORMATION

-

- I bought my home last year, and this year the taxes increased dramatically, even though I applied for the Homestead Exemption. What happened?

-

Under Florida Law, all exemptions and assessment caps possessed by the prior owner must be removed on the January 1 after a change of ownership. The prior owner was likely benefiting from a Save-Our-Homes cap benefit that held the Assessed Value of the property well below its Just/Market Value. When you crossed your first January 1 under your ownership the Assessed Value reset to Just/Market Value. We then apply any portability from a prior Florida homestead and any additional exemptions, if applicable.

- Why are my taxes increasing when the market value of my home is going down?

-

There are a couple of reasons why this may happen. It may be because the millage rate (tax rate) determined by local taxing authorities is increasing. Another reason may be what's known as the "Recapture Rule". In short, if you have the Save Our Homes cap on your property and your market value decreases, the assessed value will still increase by the annual cap rate until it reaches the just/market value.

- I have the homestead exemption, so why did my property's assessed value increase more than the 3 percent cap?

-

The assessed value could have increased by more than 3 percent for one of several reasons. If this is your first year receiving the homestead exemption, the assessed value will equal the just value. The assessed value will be capped next year and going forward. If you made any changes, additions, or improvements to your property, that portion is assessed at just value in the first year. If all or a portion of your property is not homestead property, the 3 percent cap does not apply. A 10 percent assessment limitation applies to non-homestead property. Please contact our office and speak to our friendly and knowledgeable customer service representatives for specific information about your property's assessed value.

- Why did the living area of my home decrease?

-

The living area of my home decreased on the Property Appraiser’s website. What happened?

The 2024 hurricane season brought unprecedented damage to many homes in Pinellas County. It also resulted in a better understanding by Building Officials of how the National Flood Insurance Program (NFIP) works in conjunction with FEMA rules for homes located in a Special Flood Hazard Area (SFHA), which are homes located in Flood Zones A and V. Specifically, homes built in 1975 or later and located in SFHA may not have heated/cooled living area below the Base Flood Elevation (BFE), except for a small area used to access the living areas above BFE from areas below BFE.

In order to distinguish between living and non-living areas of a home, the Property Appraiser uses the term “sub-area” to identify different areas of a home based on level of finish. Examples of sub-areas include: heated/cooled space (BAS), upper story finished (USF), finished garage area (GRF), and many more.

When a home built in 1975 or later and located in a SFHA has finished heated/cooled space that is located below BFE, that area is assigned the LAF (Lower Area Finished) sub-area in the property appraiser’s database. Prior to July 1, 2025, LAF was included in the square foot calculation used to generate a home’s living area in our database. However, after July 1, 2025, LAF was removed from a home’s living area calculation to align with Florida Building Code, FEMA requirements, NFIP criteria, and local building department building codes and permitting requirements.

This practice is consistent with how Realtors and private sector appraisers handle the living square footage when listing and valuing property since the area below BFE is uninsurable.

If the living area assigned to my home is smaller, will I get a tax refund?

In the Property Appraiser’s computer system, the value assigned to the LAF sub-area is not changing as it carries contributory value; therefore, no refund is needed. The LAF sub-area is still part of the gross area of the structure and was already valued at less than the base living area. If your value changed this year from the previous year, it was due to other factors such as an additional year of depreciation, special storm depreciation related to storm damages or other calamity, a change to the model used to value residential properties, or a change in market conditions such as higher or lower sale prices of similar properties. If your lower level was finished as conditioned space pre-storm but was returned to only parking, storage, or access after repairs, please call our office at (727) 464-3207 and ask for your Area Appraiser so that we can make the appropriate adjustments.

How do I request this area to be changed?

Your Area Appraiser is here to help and is glad to review any pertinent documentation you can provide. The primary source of information is found on an Elevation Certificate (EC) issued by a survey company, which shows the Base Flood Elevation (BFE) and the lowest finished floor height of the subject property. This is typically labeled as the “Top of bottom floor” on an EC. Another potential document that may show this information would be the architectural plans. Supporting documentation that the LAF was built above the BFE at the time of original construction would allow us to move this area back into the living area calculation. Also considered would be a letter from the Chief Building Official in your local jurisdiction stating that the LAF in question could be legally permitted for repairs as finished living space in the event of a future calamity and is insurable through the National Flood Insurance Program (NFIP).

A portion of the LAF is actually used as access to the upper floor(s). Can I have my Area Appraiser measure this area to reflect the portion that is used to access the upper stories?

Yes, your Area Appraiser would be glad to assist in remeasuring the LAF. The re-measurement will require architectural plans or an inside inspection of the LAF area to determine the size of the area used for access, which is typically added to the total living area. You may contact our office at (727) 464-3207 to schedule an inspection. If you have a copy of the architectural plans in PDF format, you can email those to our office at mike@pcpao.gov. Please include your contact information and the parcel number in the email together with your request.

Resources to Assist in Verifying if LAF was compliant at time of construction:

1. Check for an Elevation Certificate (EC) on the pcpao.gov website:

- The above EC information is pulled from the Pinellas County Enterprise GIS system: https://pinellas-egis.maps.arcgis.com/apps/webappviewer/index.html?id=c66f8a2216d34a49a9675ecaf134a61a

2. Historical Flood Insurance Rate Maps (FIRMs) can be found at the FEMA Flood Map Service Center: https://msc.fema.gov/portal/advanceSearch

- This is helpful when trying to identify what the legal BFE was at the time of original construction.

- What happens if the real estate market goes down?

-

Florida law sets January 1st as the assessment date each year to determine both value and exemption eligibility. While January 1 is the date used for setting the assessed value for the Notice of Proposed Property Taxes sent in August and tax bill sent by the Tax Collector in November, the value is based upon the market value for similar properties in the same or comparable subdivisions during January 2 of last year through to January 1 of this year. With that in mind, if sales indicate that market values have increased or decreased last year, it will be reflected on this August's Notice of Proposed Property Taxes. If a property received damage from a storm or other catastrophic event that was not repaired as of January 1 following the event, the value of the improvement will be adjusted downward to reflect the estimated damage as of January 1 of that tax year.

- Will my taxes increase if I transfer my property into an LLC, even if I own the LLC?

-

Potentially, yes. A limited liability company (LLC) is considered distinct from its owners or members. If you transfer ownership of the property in or out of an LLC, any non-homestead or homestead Save Our Homes cap benefit will be removed the following tax year as of January 1. A change in property ownership will effectively "reset" the capped value to full market value. It is important to know that property taxes will increase the next year as the assessed value must be adjusted to equal the current market value.

- How can you say that my property is worth $150,000 when I paid $250,000 for it three years ago?

-

The current valuation reflects changes in the real estate market since the property was purchased 3 years ago. Sales that have taken place since then indicate that the market value of the property has decreased.

- What should I do when I receive my Notice of Proposed Property Taxes (TRIM) around the third week of August, and I believe that the proposed value of my property is incorrect?

-

If you believe your proposed value is higher or lower than market value on January 1st, we encourage you to call our office and speak with your area appraiser who is happy to discuss your value. Often this discussion will quickly resolve any issues. Our goal is to determine that your property is appraised equitably and accurately.

If you are still dissatisfied after talking with a Property Appraiser employee, you may challenge your value or exemption status by filing a petition with the Value Adjustment Board (VAB). The VAB is the independent decision-making authority when there is disagreement between the property owner and Property Appraiser’s office. Petitions are easily filed online with the Clerk of the Circuit Court and Comptroller at http://www.mypinellasclerk.org/vab for a nominal fee.

- Can you win a reduction before the Value Adjustment Board?

-

Yes, you can if you prove that your appraisal exceeded market value. However, if you base your petition on a personal hardship, such as living on a fixed income or an inability to pay any more taxes, the unfortunate answer is "no". However, you may be eligible for the tax deferral plan administered by the Tax Collector's office. Information regarding the plan is included with the tax bill you receive in November. The fact that your value increased from last year to this year is not a basis to reduce this year's appraised value, since each year's assessment stands alone.

The Value Adjustment Board does not set the millage rate and has no jurisdiction over taxes. The only questions the Special Magistrate determines is whether the appraised value of a property exceeds its market value as of January 1, and if you were qualified to receive an exemption to which you were denied.

- My insurance company just appraised my house. Why does it differ from my TOTAL market value?

-

An appraisal made for insurance purposes does not include land and typically does not include depreciation.

- What is the Save Our Homes amendment, and how does it affect me?

-

The Florida Constitution was amended effective January 1, 1995, to limit annual increases in assessed value of property with Homestead Exemption to 3% or the amount of the Consumer Price Index, whichever is lower. However, no assessment shall exceed current market value as of January 1 of the respective tax year. This limitation applies only to property value, not property taxes.

For more details, visit Learn About / Save Our Homes.

- What is "Highest and Best Use"?

-

This term refers to the 'use' which will generate the highest net return to the property over a reasonable period of time based on current market conditions. For a more detailed explanation, visit FL Statutes Governing Assessments to learn more.

- How is land valued?

-

Land is valued using the sales comparison (a/k/a market) approach. The location of the land is a major factor in determining its value, (e.g., land located near the water is generally more valuable than inland parcels). Sale properties are analyzed and compared. Units of comparison such as price per square foot, acre, front foot or unit as determined from sale properties are most often used to arrive at appropriate indicators of value to apply to non-sale properties based on their comparability and highest and best use.

- What guidelines does the Property Appraiser follow in determining property value?

-

The Property Appraiser and staff must abide by the Florida State Constitution and the Florida Statutes. The Florida Department of Revenue also issues a manual of instructions which conforms to the intent of the previously mentioned documents. The office also ascribes to the practices and standards of the International Association of Assessing Officers (IAAO).

- What is my property value?

-

Using the Quick Search feature on our Home page, locate your property then scroll down to the Value History. Both current and historical value information is displayed for easy viewing.

Your Property Value is comprised of Land, Building, and Extra Feature values. The allocation of the property value between these three components is indicated in the FEMA/WLM Letter obtained from the Quick Pick Tool.